Beschreibung

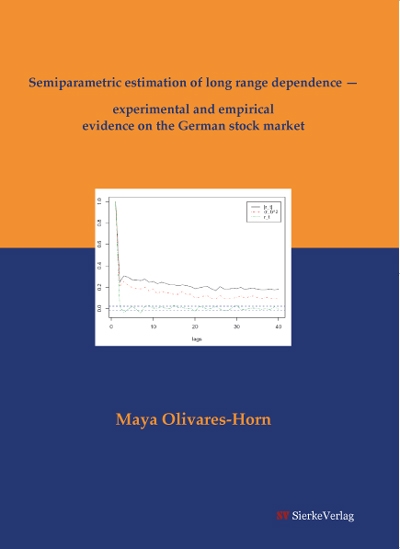

This thesis consists of the following original working papers: 1. Semiparametric Inference and Bandwidth Choice under Long Memory: experimental evidence Co-authored by Prof. Dr. Uwe Hassler, submitted. 2. Long Memory and Structural Change: New Evidence from German Stock Market Returns 3. Long memory in volatility of DAX stock returns